A strong re-emergence of rental and pay-per-use software models signifies that the industry is living in an era of contrived dynamic prosperity, not an imminent threat. Most incumbents will find a way to make hay while the sun lasts. Only Salesforce itself can tell us how long the stay of execution will last.

The force of a one customer strategy

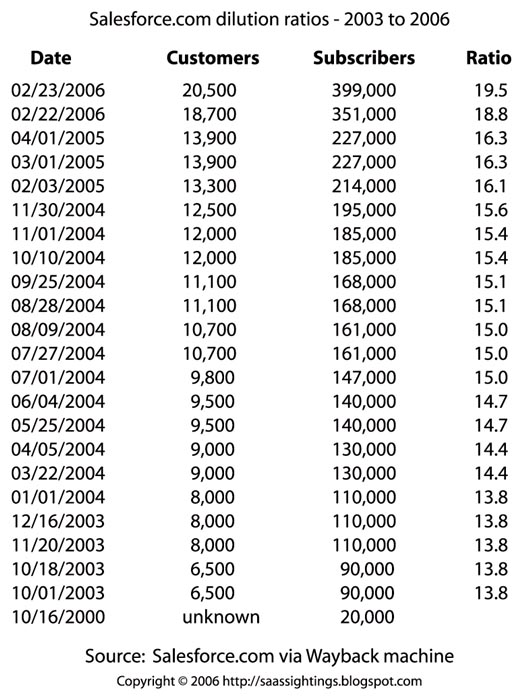

On 23rd of February 2006, Salesforce dot com, poster child of the SaaS (“Software as a service”) movement, announced 399,000 subscribers (users) across 20,500 customers (enterprises). That’s 19.5 users per enterprise. Does that tell us anything?

IT-insiders report that Salesforce has grown rapidly. The company reported earnings for the fourth period ended January 31st rising 66% to US$5.96 million, or five cents a share, from US$3.59 million, or three cents a share, in the year-earlier period. Revenue rose 67% to US$91.1 million. The company predicted revenue in its current fiscal year will hit US$470 million to US$475 million, up as much as 53% from the year ended in January.

So who the heck are Salesforce customers?

Amazon targets the average book Joe, and has extended that lead to DVDs, electronics, apparel and more. Who’s the target for a CRM app? Fortune 500 companies? Mid-market firms? Small-to-medium sized business (SMBs)? Mom and pop shops? All wrong. Salesforce.com targets just one person, the sales guy. In SaaS-lingo that’s a “one customer” strategy.

The theory behind “one customer” is this: Do it right, generalize a SaaS solution for the 1-to-many “Long Tail” mass-market, and all sales guys will sign-on. Subscribe online at a browser near you, bring your colleagues to the party and hey presto, the Sales Team are finally sharing data and (whether the CIO likes it or not) Acme Corp. has a new enterprise app. Now all there is to worry about is that pesky little process called total user adoption: encouraging the rest of the sales organization to follow suit. And if that’s a sweat, no sweat: call Salesforce adoption and consulting partner Blue Wolf Group.

So just who the heck are Salesforce customers? Sales teams who use the simplicity of SaaS to bypass corporate IT or Sales Directors blessed by Corporate IT who proactively choose the Salesforce brand of CRM as an enterprise standard? Fact is, no one other than Salesforce knows.

Let’s go Wayback

Unless you are an avid Salesforce.com groupie you won’t have been watching the company’s WWW home page for the last six years. Fortunately the Wayback Machine, another marvel of the Web, has. A little work yielded:

The dilution ratio, the average number of users per customer, is a reasonable measure of whether Salesforce is penetrating larger firms. If the NO-SOFTWARE company’s subscriber base continues to grow, and the ratio declines or increases only slowly, we can be sure that the company is appealing to the SMBs and Mom and Pop shops – even if Salesforce do manage to retain a few brand name customers. Only if the ratio increases sharply can we be sure that Salesforce is a potential bomb to companies like SAP and Oracle.

SaaS is a channel, the market is for Services

Unlike books and shoes, IT services are not so easy to segment. Will a “one customer” model work at scale amid the Fortune 500 firms? Corporate IT exists because Fortune 500 firms are creatures of process, not chaos. Would a global enterprise survive more than a few weeks if staff were left to choose-and-use the needed IT services piecemeal? Yet even if Salesforce never makes it to the SAP-GE league, the company could still enjoy a healthy business serving the Long Tail, as do Yahoo, Google and Amazon. This schizophrenia is one factor that attracts IT-watchers towards Salesforce.com in particular and to the SaaS-trend more generally. It’s a dilemma that industry analysts have yet to explain. (There’s nothing wrong with the little guy, but industry analysts typically don’t sell to them.) However, the same schizophrenia is also a dilemma for former Oracle executive and Salesforce CEO Mark Benioff. If his CRM baby doesn’t appeal to the Fortune 500, CRM alone won’t cut it as a business model among SMBs. There are already a host SaaS-CRM alternatives out there, with lower per seat costs and, some say, a more appropriate solution for small firms.

And that’s only the beginning of possible problems for the “no software” concept. Fact is: the fate of a company like Salesforce is inextricably linked with the fate of the entire software-as-a-service sector.

Most businesses, even smaller ones, need a lot more IT than CRM. If they can’t get all of the IT services they need as SaaS, CRM as a service makes no effective difference to their IT costs and IT management headache.

In “Software as a service: Pay as you build, but at what cost?” Ephraim Schwartz got to wondering in Computerworld “what if you were committed to the SaaS architecture and needed all 160 programs to run their business properly? With an average service fee of US$50 per user per month multiplied by 160 plug-ins, you get US$8,000 per user per month. Multiply that by 12 months and a dozen users and it comes to US$1,152,000 a year.”

Schwartz’ estimate of 160 is the number of services a typical mid-sized firm might need to subscribe to in order to enjoy the equivalent of a mainstream enterprise “on premise” software solution. It is based on the fragmentation of the SaaS space today, where each service is supplied by a different firm. His conclusion: “SaaS providers will very quickly face the reality that unless they are a provider of a major service with broad reach, they will not be able to charge even US$25 every month for each user. Expect prices for nice-to-have utilities to drop as low as US$5 per seat each month.” And don’t expect the problems to stop there. While many companies will adopt discrete services, integration, aggregation, consistent user interface and a host of other factors will force the emergence of SaaS channel providers, who will integrate at the backend, and the front end of the services supply chain.

Is Salesforce a force?

With doubt over Fortune 500 credentials, pressure from online CRM alternatives and a CRM-is-not-enough business case even among SMBs, it’s no wonder that Salesforce has launched AppExchange.

Working with ISVs, the company is extending its value-proposition by offering related or complementary applications. Can Salesforce capture the SMB business-IT service chain? Technically, it’s possible. And no doubt the company has a sophisticated model for wresting further revenue per user based on take-up of additional service via AppExchange. Indeed, March 6th 2006, Salesforce upped prices for Fortune 500 premium services, by nearly a factor of four! The move is the latest step toward delivering bundled services beyond customer relationship management (CRM) “Front Office” applications. Analysts said it could help Salesforce.com compete against bigger rivals Microsoft Corp., Oracle Corp. and SAP AG by providing tools to make building out platforms and deploying related applications. And Salesforce provide tools to integrate back into on-premise core systems – which are unlikely to fall under the SaaS hammer.

Could it be that AppExchange is a signal that executives at the firm concluded a year ago or more that the original CRM-only play was unviable unless more sizeable firms signed-up in scale. With a weak dilution ratio, and unless AppExchange becomes a “destination” on the scale of Google or Amazon, it’s curtains for Salesforce.com as poster-child of the much-talked-about “disruptive” transformation of the large enterprise software economy signaled by SaaS.

Look at Amazon. What began with books, expanded to Videos and DVDs, then to toys and electronics, onto apparel, fashion accessories, beauty products, gourmet foods, jewellery, shoes, musical instruments, health products, furniture, bed and bath, kitchen ware, pet suppliers, tools and automotive.

Categories at Amazon expanded wildly not just because it was possible to ship them from the warehouse, but because other online retailers would quickly erode the business case for a niche “books only” Amazon. The same will be true of Salesforce.com, once selling software begins to resemble selling any other form of online content.

Who cares who pays?

The problem for Benioff and team is that on every conceivable podium they cannot resist touting the brand-name customers they have picked up. Like the intro to a Star Wars movie, the latest names scroll up and fade into the distance on their home page.

Many of the company’s executives spent the earlier part of their working life amid Big Iron IT, a world dominated by cash-rich IT spenders eager to wrest competitive advantage from protracted “on premise” enterprise software projects. So far, Nick Carr is wrong, it’s not yet the end of Corporate IT. Those projects are, and were, deeply dependent upon veritable armies of consultants to customize and adopt software to fit unique business processes. (look to BPM for help) Hats-off to Salesforce for trying to disrupt a status quo, but the simplicity of one-click sign-up to CRM belies a greater complexity. As Nick Carr has pointed out, IT “no longer matters” if equivalent IT is equally accessible to all. Will Fortune 500 CIOs value Salesforce or its equivalents when Mom and Pop can sign-up on the same terms with one-click? Does the SaaS model by design drive towards commodity?

When the Fortune 500 adopts commodity services, they will be valuing commoditization, not differentiation. Just as quickly they will move onto new territory, areas of IT where they can differentiate, not corrode, competitive advantages.

And won’t they get nervous if their Fortune-listed friends aren’t also Salesforce users? If SaaS is as easy as people say it is won’t there be a host of options in the market. Already there are SaaS-enablers offering an “easy as 1-2-3” process: 60 days to SaaS: Wrap, Host and Serve.

And what will SMB firms think about subsidising larger firms so that they can enjoy a low cost of instant-on rental software? Won’t Salesforce be forced to find ways to extract even more cash from the cash rich?

Who has the Force?

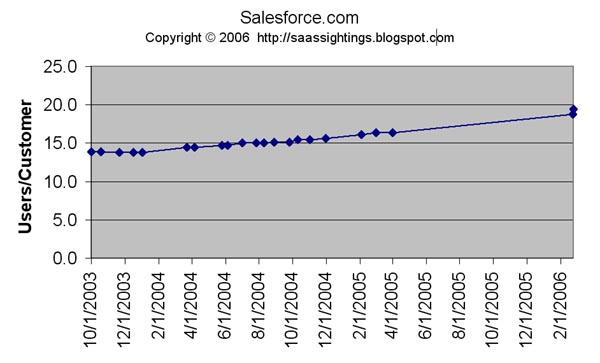

Business may be moving at SalesForce.com, but it is moving slowly. Since October the 1st 2003, the dilution ratio has increased by only six, from 13.8 to 19.5. The chart is near linear over the range.

A slight jump at the end of February 2006 may signify that existing customers are adding seats. Alternately it may just be a delay in publishing or tallying figures to coincide with earning press.

No doubt Salesforce does enjoy a small number of “showcase” brands among its 20,500 “customers”. No doubt some “customers” have hundreds, or even low thousands, of users. Even so (and assuming linear growth continues) Salesforce does appear to be playing firmly in the SMB and Mom and Pop Shop markets. Watching Benioff on-stage make hay of the brand names that, as the company says, “have the Force”, one cannot help that queasy feeling that even wins might be a push once SAP and Oracle get their SaaS act together.

More demographic information is needed before final conclusions are drawn.

Building out scale

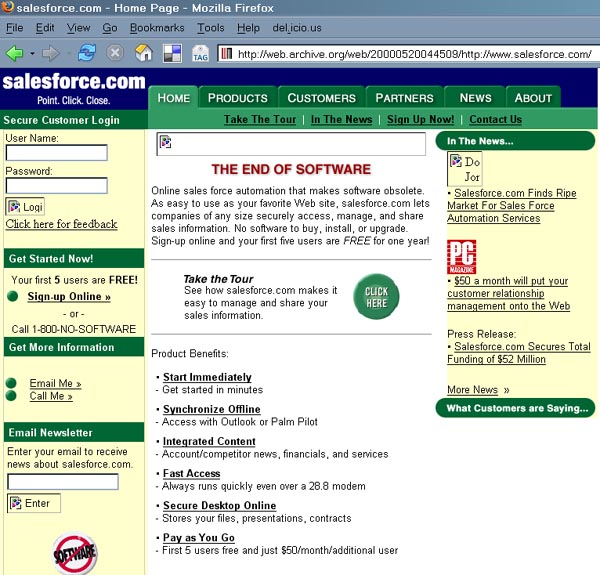

An image of the Salesforce.com home page from May 2000 is revealing.

One year in, the start-up had raised US$52 million in venture capital investment. At the time, rental of the CRM app would set you back $50/month/user. The company was giving away five free users to drive adoption. Today, rental is $65/month/user, with discounts for volume. That’s six years to drive per seat cost $15/month. (putting side the recent 4x increase for premium “Fortune” service)

Assuming all users pay the full $65 (which is unlikely), today’s 399,000 subscribers bring in US$25,935,000 per month. That is the equivalent of a typical Fortune 500 enterprise-IT project each month. Those companies have serious IT-work in their markets. But it’s nothing to do with CRM. Aerospace, healthcare, finance, government and biotech don’t “run on CRM”.

Twelve projects a year is hardly a market disruption. And with pressure on per-seat costs growing among CRM competitors, SaaS announcements starting to flow from incumbents getting into the game and an urgent pressure to build out beyond CRM, Salesforce is hardly done and dusted.

Is Christensen’s model appropriate?

The debate about SaaS raging in the Blogosphere will no doubt be informed by the progress of Salesforce. Analysts IDC are making some noise.

IDC have a partnership with Innosight – the strategy firm founded by disruptive innovation guru Clayton Christensen. The group has virtually announced that SaaS signifies a classical Christensen disruption. The innovation guru’s name, and the term SaaS, appear on at least one Web page.

According to the theory, SaaS targets overshot customers in less-demanding tiers of a market with a “good enough” product or service at lower price point. Signals of overshot customers include: people complaining about overly complex (“On premise” software – “armies” of consultants) and/or expensive products/services (“SAP license upgrades”) and features not getting used/valued (software licenses “sitting on shelves”, 85% of software package features irrelevant to most users). Sounds plausible?

Drawing analogies with Salesforce, analysts are pointing towards other “disruption indicators” giving credence to the theory. These include the emergence of a “different” business model (rental, pay per use), “new” technologies (AppExchange “platform”), simplified cost structures (“customer of one” – no need for sales staff) and fluid distribution systems (Web service chain) that add up to attractive profits at lower price points.

It is possible to point to other “litmus tests” as evidence that the IT industry is undergoing a significant change with SaaS. For non-customers (enterprise business units waiting for applications Corporate IT have failed to deliver), does the product or service (“SaaS marketplace”) help customers accomplish an important, unsatisfied job; or is success predicated upon their wanting to get done something that historically hasn’t been prioritized? Or does it (SaaS) compete against non-consumption – enabling a larger population of less-skilled or less-wealthy people (“business users without IT skills held captive by IT departments”) do things that previously had not been possible? All roads seem to point to a disruption: but to whom?

With SaaS and Web 2.0 announcements now flowing from virtually every ISV on the planet (http://saassightings.blogspot.com) does Salesforce even matter any more as a barometer of the SaaS trend? In so far as the company is a litmus-test of a Christensen disruption, yes. If the movement’s poster child fails to penetrate the Fortune 500 at scale, or only appeals to smaller enterprises, SAP and their ilk, together with their extensive networks of after-sales services and support, can sleep easy in the knowledge that monolithic, bloated and over-priced offerings are safe, for a while. If, on the other hand, Salesforce only succeeds among large firms and fails to reach out to the little guys, it and similar offerings can be viewed as “just another app” and the new technology of AJAX and Web 2.0 as little more than a fancy-browser front-end (remembers XWindows). In such a case, the software manufacturers will be unaffected, but consultants had better embrace off-premise development and evolutionary development methods. Vertical integration between content, service and consultancy will be the mantra if SaaS succeeds.

The real Bomb for the IT industry would be if the “one customer” strategy succeeds and the Salesforce subscriber demographic (via the dilution curve) signifies universal appeal – the Flower Shop and GE – evenly distributed. In this case, and in this case alone, CEO Mark Benioff will have cast a fatal blow and triggered a genuine new software economy. That data is not yet in. Everyone is biting their nails.

So until Benioff and team publish more demographics, there remains a doubt over whether Salesforce is a Christensen disruption (Threat to incumbents, Opportunity for the new guy) and if so, to whom. Where there is no doubt is that the IT industry is now living in an era of contrived dynamic prosperity.

Living on borrowed time

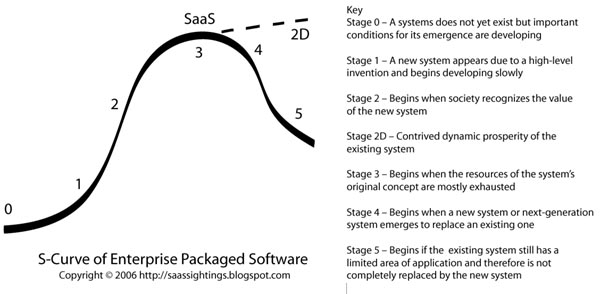

Contrived dynamic prosperity is an aberration of the standard S-curve of organizational and technological development. It’s a state in which the threats and opportunities surrounding an innovation play against each other, orchestrated by old and new players in the market: those who seek to save the status quo (SAP, consultants etc.) and the other seeking to change it (i.e. Salesforce, SaaS models).

Contrived dynamic prosperity prevents the natural aging of incumbents and assures the achievement of the desired lifecycle of the organization, that is, sustainability through growth, defying stagnation in stage 4. Growth as a result of contrived prosperity is rarely dramatic, but it remains reliable. In addition to the existing hierarchy of control (the “on premise” IT orthodoxy pre-Salesforce), an inverted hierarchy emerges that is required to control, cooperate with, and oppose (within limits) the up-start (i.e. “customer of one”).

The business leader in the time of contrived prosperity usually understands and accepts the prevailing incumbent internal and industry culture and does not attempt to replace it, rather, they attempt to work it to their advantage. A recent example can be found in the SaaS announcements of IBM.

IBM is trying, but will fail, to control the SaaS movement by expanding its resource allocation to application partners keen to embrace SaaS and so drive revenue to its own applications hosting businesses. No doubt revenues will be generated, but if SaaS is real, control it you cannot (as Yoda who really does have the force, would say).

IBM is boosting the number of its ISV partners via a “SaaS showcase”, implying that offerings from elsewhere (i.e. the Web) are somehow inferior or risky. They are not. IBM is offering incentives through its extensive business networks to entrap deals at the earliest stage and drive a focus and attention to its own hosting/provisioning services. Access to local IBM sales staff is promised to “add credibility” to SaaS-vendor sales efforts going on in among IBM target customers. This has, for some time, included the mid market.

Having moved out of the applications space, IBM is now encouraging adoption of SaaS by providing ISVs access to its sales staff to help close deals that result in a slice of IBM revenue. The company has opened “virtual innovation centres” to provide guidance to intellectual property owners (software firms) on how to make their offerings available in the IBM On-Demand environment. In a quid pro quo, IBM is offering its own direct mail and telemarketing resources to ISVs moving to SaaS in order to help them generate leads, leading of course to further take up of IBM hosting. Workshops by IBM architects are already touting the advantages of the SaaS model (remember SOA) and advising ISVs on software transformation, service-design and security implications. Buyer-beware: an initiative to develop standards for SaaS interoperability has begun.

IBM’s defensive moves to control SaaS are one signal that, unlike the previous era of failed Applications Services Providers (ASPs) who never cracked the multi-tenant architecture, the industry has, this time, entered the contrived dynamic prosperity stage of its evolution. It’s not the "end of software" Mark, but it might be an end to complacency.

Come on Salesforce, publish the Demographics Force. Mean, mode and medium please, Mom and Pops, Small Enterprise, Mid Market, Global 5000 and Fortune 500. We’ll then know more about how long this new and troubling stage in our industry is likely to last. Are you the Bomb, or will you Bomb-out in enterprise markets even if you succeed to be IT-Guy to the little guy?

Copyright © 2006 Howard Smith

4 comments:

Great posting!

How do you think salesforce.com's prospects look in Europe and Japan? Do you think SaaS has the same potential in Europe?

Howard, I think you are asking the right questions about Salesforce.com. However, I am not sure I would agree with your take on the distruptive nature of SaaS.

Making a product or service available to the "great unwashed masses" at a disruptive price point usually increases the total available market for that product -- exponentially. Remember the PC twenty years ago? The enteprise IT shops (and their incumbent vendors) laughed at the PC and called them toys for about 10 years, while small companies and departments of Fortune 500 kept buying them. At the end, the PC became "good enough" - today, most Fortune 500 dacenters are full of Intel servers, while Sun is wondering where did their market go.

For an example from a different industry, consider Southwest Airlines. 10 years ago, a lot of analysts were making a case similar to your case with Salesforce.com - that in the airline business, the real money is in the business traveller who is willing to pay a premium, bla bla bla, and Southwest cannot be a real airline without a business class section & perks, an airport lounge and a frequent flyer program. Fast forward to 2005, the incumbent airlines are all operating under bancrupcy protection, while Southwest is the healthiest airline in the US - still without a business class. No lounges, either... But they got the frequent flyer card. What happened to the busness traveller? These days, 90% of the execs and salespeople I know take Southwest for any flight that's shorter than 2 hours. Why? Saves you about an hour door to door, easy to hop on the next flight if you need to spend an extra half an hour with a customer... and you can't beat the price, of course.

Also, look at Intuit which started with mom and pops in 1993. Their QuickBooks was a great tool for tiny companies... in 10 years, Intuit pretty much took over the accounting software market and the tax preparation software market. In 2006, they are busy killing H&R Block. No Fortune 1000 accounts (yet), but the rest of the world is theirs.

So the key question I would ask about Salesforce.com in this context is not whether they can suck the bloated IT budgets of Fortune 1000 today, or even in the next 3 years (if history is any indication, they will not be able to - yet). The real question is whether they are instrumental in growing the CRM user base beyond the few companies that can afford SAP and Siebel. If they are, the future is theirs. Who needs CRM outside Fortune 1000 companies? Who doesn't? Every company that has at least 2 salespeople and a CEO needs a CRM... at the right price point, and easy to use.

Eventually, the SaaS apps will become "good enough", and take over the Fortune 1000 users. While SAP and Oracle continue to retreat upmarket, serving smaller and smaller customer base with increasingly unique requirements. Just like the mainframe. BTW, IBM still sells about $8 Billion a year worth of mainframe products. But, who cares?

Howard, I'm not sure why you are calling this Dilution Ratio. I think it would make more sense to call it Concentration Ratio. In any case, I can't see that slow growth in concentration is such a problem for SalesForce. I discuss this further at SalesForce adoption.

With the high churn some analysts believe exist with salesforce.com (30% - 38% depending on the analyst, I think it is the small guy who is leaving and that's what is pushing their average up. Recall that when they started there were no other options. But there are many other options today that are more affordable. So in the end we'll see who the Salesforce.com customer is...I noticed that Entellium is on Verizon Wireless' site so there is competition for the small guy out there.

Post a Comment